Top Stories

Corbynite Economics

In many ways, it is a book that feels badly out of date, and it is unlikely to be of interest to many people beyond those who already agree.

{kind=link}

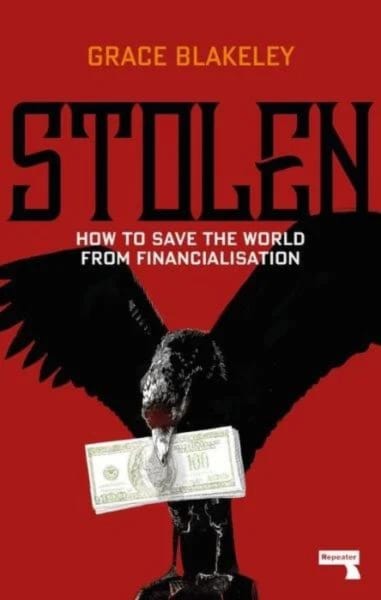

A review of Stolen: How to Save the World from Financialisation by Grace Blakeley, Repeater Books (September 2019) 300 pages.

It is tempting for Jeremy Corbyn’s critics to write off his electoral promises as bribes—a last-ditch attempt from the most unpopular major party leader in memory to buy his way to victory. There’s some truth to this when it comes to pledged levels of public spending. But Corbynism is not an opportunistic ideology. He and the people around him have a set of beliefs about the economy that they take very seriously, and it’s worth trying to understand them.

Stolen: How To Save The World From Financialisation, by New Statesman columnist and socialist campaigner Grace Blakeley, is one of the more serious attempts to set out a version of Corbynism (compared to, say, Aaron Bastani’s buffoonish Fully Automated Luxury Communism). Blakeley, who recently tweeted that reading the Labour manifesto had moved her to tears, has tried to put modern leftism in a post-financial crisis context. Her book hopes to explain why she believes the crisis was the inevitable consequence of Thatcherite neoliberalism, and why now, more than ever, the time is right for socialism.

I’m halfway through the manifesto and I’m not ashamed to say I’m in tears.

This isn’t just a plan to take on the powerful, it’s a plan to rebuild our society from the ground up – a collective vision for a better future that we will work together to build. https://t.co/37fb7JLCq5

— Green New Deal Now Blakeley (@graceblakeley) November 21, 2019

Blakeley focuses on what she calls “financialisation,” a term that means different things to different people but which she takes to mean the use of private financial markets as the dominant mechanism for allocating money for lending and investment, instead of, say, government agencies. She blames the rise of finance for two related evils: one, diverting investment away from industrial production towards speculation on things like housing and company shares, and two, bond markets forcing governments to adopt free market economic policies, or face higher borrowing costs.

Her story begins at the 1944 Bretton Woods conference, at which delegates from the Allied nations, including a British delegation led by John Maynard Keynes, designed the system of global currency that would last for thirty years. What they came up with was a loose peg to gold intended to prevent sudden large fluctuations in exchange rates but allow more flexibility than a true gold standard. This, according to Blakeley, kept financial markets in line by preventing large capital outflows and by restricting the supply of credit. This allowed the “Keynesian consensus” to emerge—a sort of moderate, worker-friendly capitalism characterised by generous government spending, an economy based on manufacturing output, and strong unions that could maintain some balance between the interests of workers and capital-owners. Not a Marxist’s paradise, but hardly the stuff of nightmares.

That didn’t last long. In the early 1970s, the oil crisis hit, Bretton Woods was abandoned, and true capital mobility arrived—what Blakeley calls “vulture capitalism.” The Keynesian settlement became a victim of its own success, with unions capturing so much of the product of industry that capital-owners “revolted” and pulled their money out of places like the UK, leading to industrial strife that eventually brought Thatcher’s radical free marketeers to power. Blakeley only spends a few pages on the 1970s, even though this was precisely the point where everything, from her point of view, started to go wrong. The 1970s, she argues, highlight the “contradictions of social democracy,” because as unions grew in power, capital-owners still had the freedom to move their money elsewhere. (Readers with a deeper knowledge of the strikes and shortages that led voters to gamble on Thatcher may find Blakeley’s version of events to be less than the whole story.)

Under Thatcher, Blakeley’s thesis takes shape. By encouraging mortgage-funded home ownership and bringing in the “Big Bang” deregulations that led to the growth of the City of London as one of the centres of global finance, Thatcher’s government began the financialisation that Stolen purports to be about. Blakeley believes that Thatcher’s crushing of the unions was what made this possible: “Without resistance from the country’s workers, she could go about entrenching neoliberalism and empowering the financial elites that had brought her to power.” Debt rose, asset prices grew, and the financial sector became responsible for allocating more and more resources across the economy. Without state support, and with capital now being allocated according to profit-obsessed financial markets, industry across much of the UK collapsed. As more and more voters became property-owners, their interests shifted from being aligned with workers to being aligned with capital.

We then skip ahead to 2008. After twenty years of growth, which Blakeley describes as largely “illusory,” the bubble bursts. House prices, which had risen and risen thanks to easy borrowing, fell sharply in much of the developed world. This caused banks that had lent money for mortgages, and others that had repackaged those mortgages into tradable financial instruments, to collapse. The bubble burst, the system (almost) collapsed, and the inherent contradictions in debt-financed capitalism were exposed for all to see. It was these developments that precipitated the landslide election of lifelong socialist backbencher Jeremy Corbyn as leader of the British Labour Party in 2015.

If that story sounds new to you, Stolen may be a useful book. It offers a fairly readable account of this account of postwar economic history, and it does so at a brisk pace. If, on the other hand, you have some cursory knowledge of the events of 2008 and the years that followed, much of it will feel reheated and oversimplified. Blakeley repeatedly digresses into discussions about some aspect of Karl Marx’s thought, and why the events she has just described demonstrate that Marx was right about something or other after all. In the first chapter’s explanation of Marx’s theory of history, she describes a debate within Marxist circles about whether “Marx prioritised economic structures in his analysis of historical development, [or whether] he prioritised agency.” It turns out he believed in both: “the nature of technology and the economy provides the overarching context in which human action takes place … But they do not determine human action.”

This is a surprisingly anodyne version of Marxist history. Does anyone disagree that “Men make their own history, but they do not make it as they please,” as Blakeley summarises her mode of analysis? It soon becomes apparent that she is less interested in “financialisation” as a phenomenon in itself than she is in using a relatively recent feature of capitalism to demonstrate an old Marxist claim: that capitalism sows the seeds of its own destruction. Readers hoping to understand how finance affects the “real” economy will be disappointed. Here, finance merely plays the role that “capital” did in the nineteenth century: as the rapacious, faceless force that proves capitalism can never really be sustainable.

Blakeley’s analysis is often misleading. What she calls a housing “bubble,” in Britain and the US at least, does not seem like one with the benefit of another ten years of evidence. House prices in both the UK and US are higher now than they were in the years leading up to the crisis—when “bubbles” burst, they do not tend to return to their old values within a few years. (A house in central London is now much more expensive than it was even before its “bubble” burst. A share in Pets.com is not.) Blakeley suggests that this is just a sign of another bubble, a claim which (for now) it is impossible to make with any certainty. It seems a lot more likely that climbing house prices are driven by planning restrictions that limit the supply of housing in large cities, combined with economic prosperity that attracts new workers and higher wages with which to bid up the price of the existing stock of homes.

Tomiwa Owolade

Tomiwa Owolade

If this were not the case, and mortgage borrowing were the main culprit, we would expect to see house prices inflated by roughly the same amount across the country, not largely confined to places where people most want to live and where supply is most inelastic. In Tokyo and Houston, for example, which have relatively permissive laws about the construction of new housing, economic growth and historically low interest rates have still not led to significantly rising house prices.

Blakeley has been criticised for misusing terms like “bank capital,” which have a precise meaning that her text seems to misunderstand (she appears to be mixing bank capital requirements up with liquid assets and reserve requirements, for example). But, while these may reveal some fundamental misunderstanding of the things she is writing about, it may also be the result of hasty editing or an attempt to translate technical terms for laypeople. Much more troubling than some garbled definitions is the frequency with which Blakeley makes claims that have no basis in evidence, and for which she provides no citations.

Blakeley claims that productivity and worker compensation have decoupled, disproving a core tenet of mainstream economics—that workers will tend to be paid according to their marginal product, so strong unions are not necessary to ensure they capture a share of economic growth. But the data show no such decoupling. There is evidence that workers are being “paid” increasingly in forms of compensation other than wages, like pension contributions and, in America, health insurance contributions. But these simply change the mix of how workers are paid, and are mostly driven by changes in regulation. I may prefer to be given £1,000 in cash to an equivalent contribution to my pension, but it is hard to argue that the latter is not really payment to me.

Similarly, she claims that “people are having to work ever harder to maintain a lower standard of living.” Despite the fall in living standards after 2008, this is simply not true. GDP per hour worked may have grown anaemically since the crisis in Britain, but it is still higher than it has been at any point in history (and inequality has not risen in this period). It is just wrong to suggest that living standards are falling—but it is the sort of claim that Blakeley has to make in support of her insistence that “we inhabit a revolutionary moment.” If living standards are historically high and growing, just not growing as quickly as we’d like, the case for revolutionary upheaval is weak.

She also repeatedly makes claims about “illusory” debt-fuelled growth, including the extraordinary assertion that “during the pre-crash period, unprecedented levels of lending were the only thing keeping the US economy going.” This declaration is unsupported by a citation and has no basis in fact. The most charitable reading is that it is Blakeley’s opinion and she simply doesn’t think that certain forms of economic growth really count. But it is also circular—we know the crash was inevitable because the growth was illusory, and we know the growth was illusory because of the crash.

Stolen promises a guide for “saving the world” from this financialisation, but Blakeley’s policy recommendations do not inspire confidence. Borrowing from the recent People’s Republic of Walmart, she points out that businesses are themselves centrally planned, and so it should not be counterintuitive to run a country along the same lines. This completely misunderstands how businesses and markets work. Businesses exist within a system that is generally designed for the ones with bad internal planning to collapse as swiftly as possible. Effectively, we get to choose between the most well-planned companies and, unless we have lent to, invested in, or work for a company that goes broke, we are largely insulated from the ones that fail. (This is one reason why we provide unemployment insurance to people who do have the misfortune of working for a company that fails, and why bailing out large banks sets such a bad precedent.)

For such a system to work for entire states it would need to be just as easy for families to migrate between countries as it is for workers to migrate between employers and for consumers to choose between different businesses. In practice, of course, the unfortunate citizens of centrally planned economies have often tried to migrate away, and had to be fenced in with barbed wire, or worse. Blakeley does not discuss the real world experiences of the sort of system she proposes, but she does recognise that investor flight is as much a challenge for centrally planned economies that get it wrong as it is for businesses.

To solve this, she recommends measures that will not sound alien to anyone familiar with the bolder elements of Corbynism: capital controls on taking money out of countries, measures to regulate banks and establish a nationalised retail bank, a “Green New Deal,” a sovereign wealth fund, and part-nationalisation of industry along “democratic socialist” lines, where businesses are controlled by unions of their workers rather than capitalists. This last idea has made its way into the Labour Party manifesto, although Labour says it only wants to nationalise ten percent of each business affected, for now.

Stolen is a wasted opportunity. Blakeley’s determination to vindicate Karl Marx means that much of the book feels like it has been generated simply to add new meat to some very old bones. This is a pity: there is plenty of merit to the materialistic Marxist analysis of history, and such an approach may have added something new to our understanding of the post-Thatcher era. But there is nothing like that here. There’s very little attempt to persuade the reader of the value of Marx’s thought, either. Blakeley’s assumption seems to be that you are either already a Marxist, and therefore predisposed to regard any invocation of Marx as authoritative, or that you are totally unfamiliar with Marxism, and any other theory of history, and so a simple explanation of what Marx thought is sufficient to persuade you of his prescience.

Blakeley writes engagingly, although she leans too heavily on clichés (the “yawning” trade deficit is driven from the City’s “gleaming towers”; the “moment of crisis” she describes could also be “a moment of opportunity”). It is footnoted thoroughly, and contains an impressive understanding of mainstream analysis of the crisis—indeed, this is the book’s most informative and coherent chapter. But this also makes the rest of the book feel shallow by comparison.

Had Stolen been less slavishly devoted to Marx, and taken a narrower focus, Blakeley might have better explained her own views and their relevance to contemporary readers. But more time is spent discussing coal mining than, say, the internet and what her thesis tells us about tech giants like Amazon and Apple. In many ways, it is a book that feels badly out of date, and it is unlikely to be of interest to many people beyond those who already agree. Worse, it is riddled with exaggerations, unevidenced opinions, and dubious claims presented as indisputable facts. Halfway through, Blakeley tells us that “There is, of course, no such thing as neutral economic analysis.” Stolen is certainly evidence of that.

Keep reading

Searching for Structure

Strange Bedfellows

The Axis of Renewal

Doomscrolling into Adulthood