The Clear Case for Capitalism

At a time when socialism and anti-capitalist populism are experiencing a resurgence, this is my attempt to turn the mysterious capitalist calzone into an appetizing capitalist pizza.

{kind=link}

At dinner not long ago my daughter and I had a standoff. She refused to eat something—a calzone in this case—because it looked “gross.” I failed to convince her what was actually in the calzone until finally I cut it in half and into a triangle so it looked just like pizza. Once she learned what was in it she loved it.

I recalled this calzone a few weeks later when I got into a heated discussion with a friend. He is convinced that capitalism is the source of all of America’s problems. As the discussion progressed, it became clear to me that the source of our disagreement was definitional: we didn’t have an agreed-upon understanding of what capitalism is—or, in other words, what’s “in it.”

Perhaps this kind of disagreement isn’t surprising given that only 22 states require high school students to take a class in economics to graduate, less than 50 percent of high school students have any exposure to economics, and only three percent of colleges require an economics class (!). So I decided to compile my thoughts about what’s really “in” capitalism. I came up with three tenets that break capitalism down into something more digestible and debatable, each of which I’ll discuss further in what follows:

- Capitalism is trade, which creates wealth.

- Capitalism is competition, which spurs innovation & lowers prices.

- Capitalism is unselfish, which brings cooperation & peace. (I know, some readers will already think this is ridiculous. We’ll get there).

At a time when socialism and anti-capitalist populism are experiencing a resurgence, this is my attempt to turn the mysterious capitalist calzone into an appetizing capitalist pizza. Everyone loves pizza.

I. Capitalism Is Trade

When goods do not cross borders, soldiers will.

~Frederic Bastiat

Consider the following:

- I list a used car for sale on Craigslist for $5,000.

- A buyer shows up and offers $4,000, but he’ll buy it on the spot if I accept.

- After some negotiating, we settle on $4,500.

Who won this trade? We both did. He wanted the car more than $4,500, and I wanted $4,500 more than the car. Behind every fair trade, both parties get what they want. As a result of this simple transaction we’re both better off. And by better off, I mean we are both wealthier. To quote Paul Graham:

If you want to create wealth, it will help to understand what it is. Wealth is not the same thing as money. Wealth is as old as human history. Far older, in fact; ants have wealth. Money is a comparatively recent invention. Wealth is the fundamental thing. Wealth is stuff we want: food, clothes, houses, cars, gadgets, travel to interesting places, and so on. You can have wealth without having money…..You can make more wealth. Wealth has been getting created and destroyed (but on balance, created) for all of human history.

And once you realize this simple truth, that wealth can be created out of thin air, a few corollaries to this truth should also be clear:

- If wealth can be created from thin air, it is not zero-sum. To believe otherwise is to fall victim to the fixed-pie fallacy.

- This means that every single person on earth can be wealthy. And, as we’ll see, we’re on our way to exactly this outcome.

- Once something of value is created (i.e. ‘wealth’), it’s shared with others by selling it to them. In other words, wealth is shared via trade.

For an illustrative example of the value of trade, read about the man who tried to create a sandwich without trading for it:

Tired of free trade? A man spent $1,500 and 6 months of his life to make a sandwich from scratch. https://t.co/QOdXUE3H8h

— Human Progress (@HumanProgress) August 5, 2016

Note that this same principle—gains from trade—also applies when countries trade with each other. This is where massive wealth gets created. Through billions of transactions with other countries, either as a buyer (of imported goods) or a seller (of exported goods), global wealth is maximized. If international trade is restricted, global wealth suffers.

That is why, when foolhardy politicians promise to stop trading with other countries, or to tax goods produced by those countries, we should probably worry (who do you think ends up paying those “tariffs”?). When other countries produce goods at a lower cost (including their opportunity cost) than we can produce ourselves the result is lower prices. And lower prices mean consumers are wealthier.

The debate, however, always focuses on the loss of jobs (i.e. the negative effect on the producer) not on the gains that come from cheaper goods (i.e. the positive effect on the consumer). When President Trump promises that he’ll force Apple to produce their products in the US—and nowhere else, he reasons that America will recover jobs lost to overseas manufacturers. He couldn’t be more wrong. If Apple has to produce the iPhone in the US, what do you think happens to the price of an iPhone? It skyrockets. Pick one of the following:

- Buy a new iPhone (built where costs are lowest) for $650.

- Buy a new iPhone (manufactured in the US) for, say, $3,000.

And if we must pay higher prices for everything, what does that do to our wealth? It wipes it out. Every iPhone owner becomes poorer than they would have been otherwise. The United States is enormously wealthy as a country because we buy from the lowest-cost producer, which creates tremendous value to the buyer. Furthermore, companies that export goods to foreign buyers tend to pay higher salaries than companies that only serve a domestic market. If you simply focus on the jobs lost to the foreign producer, you miss the other side of the coin.

But, you might wonder, which side of the coin is more important? Should we worry more about the loss of jobs to foreign competitors, or should we focus more on gains that come from trading with foreign partners? To quote a recent study from the Economist:

As it turns out, protectionism (preventing trade with foreign countries) hurts consumers and does little for workers. The worst-off benefit far more from trade than the rich. A study of 40 countries found that the richest consumers would lose 28 percent of their purchasing power if cross-border trade ended; but those in the bottom tenth would lose 63 percent (because they actually buy more imported goods).

The same is true for all industries where the US cannot profitably compete. An eternal rule of economics is that countries should focus production where they have a comparative advantage, and outsource everything else.

Rather than trying to restore jobs that are better done elsewhere, we should be focusing our energy on helping those workers that are displaced by foreign competition. This is much easier said than done, especially when dealing with people’s livelihoods. But it must be done.

Capitalism Is Competition

“But there are plenty of examples of companies taking advantage of their customers!” you might say. “Doesn’t that show that capitalism is bad and that greedy executives can get rich on the back of their customers?”

Look, for example, at Mylan—the pharmaceutical company that sells the EpiPen, a lifesaving product for those with severe allergies. Mylan recently made headlines by charging $600 for a product that costs less than $20 to make. Isn’t it ridiculous that a company can charge outrageous prices for a product that saves lives and only costs a few dollars to make? Yes, it is ridiculous. And capitalism would fix it, were it permitted to do so. This brings us to the second tenet of capitalism: that in true capitalist economies, competition means companies like Mylan can’t do what they are doing with the EpiPen.

In a normally functioning free economy, seeing Mylan screw over its customers would inspire an entrepreneur to create an EpiPen competitor and sell it for $590. A competitor then does the same and sells it for $500. And so on, until profits in the EpiPen industry are eroded away by this magical concept of competition. There are a few reasons why this doesn’t happen in the pharmaceutical industry. This post from Scott Alexander provides a great overview, but the short answer is that capitalism isn’t allowed to work. Instead, corporate cronyism—a type of fake capitalism—prevails, and monopolies like Mylan form as a result. As Milton Friedman observed:

The great danger to the consumer is the monopoly—whether private or governmental. His most effective protection is free competition at home and free trade throughout the world. The consumer is protected from being exploited by one seller by the existence of another seller from whom he can buy and who is eager to sell to him.

To summarize this second tenet: when companies are forced to compete to survive (which is what happens in a capitalist economy), the consumer wins big. This is because:

- In order to compete, entrepreneurs must innovate.

- Innovation usually means newer technology.

- Newer technology often means lower prices.

- And lower prices mean consumers get to capture more of the gains.

Yes, both parties are better off in a trade, but when capitalism prevails and trades happen at lower prices, consumers capture more of the gains than they would otherwise, and total gains (the sum of consumer gains plus producer gains) are maximized. Competition pushes the world forward, as risk-seeking intelligent inventors and entrepreneurs find ever more ingenious ways to compete with larger, established companies, bringing the market lower-cost and higher-quality products.

Three quick examples:

WhatsApp vs. SMS: Before WhatsApp, AT&T and others would charge customers anywhere from two to four cents for every text message sent. This produced billions in revenue each year. Then, along came a tiny software company offering FREE UNLIMITED messaging worldwide and….boom!:

Uber vs. Taxis: I have friends who tell me they used to be unable to reliably call a cab in NYC because they’re black. Not to mention the terrible service and high prices. Along came Uber, and now….well you know. The price is lower, the technology better, and my friends get picked up. The gains to consumers (also known as consumer surplus) are off the charts.

Spotify vs CDs: My kids will never know this, but I used to collect something called “compact discs.” They contained about 12 tracks, they were vulnerable to scratches and other damage, and they cost about $20 each. Then, along came Spotify, Apple Music, and Pandora and now every song ever created is at my fingertips—for less than the price of a CD.

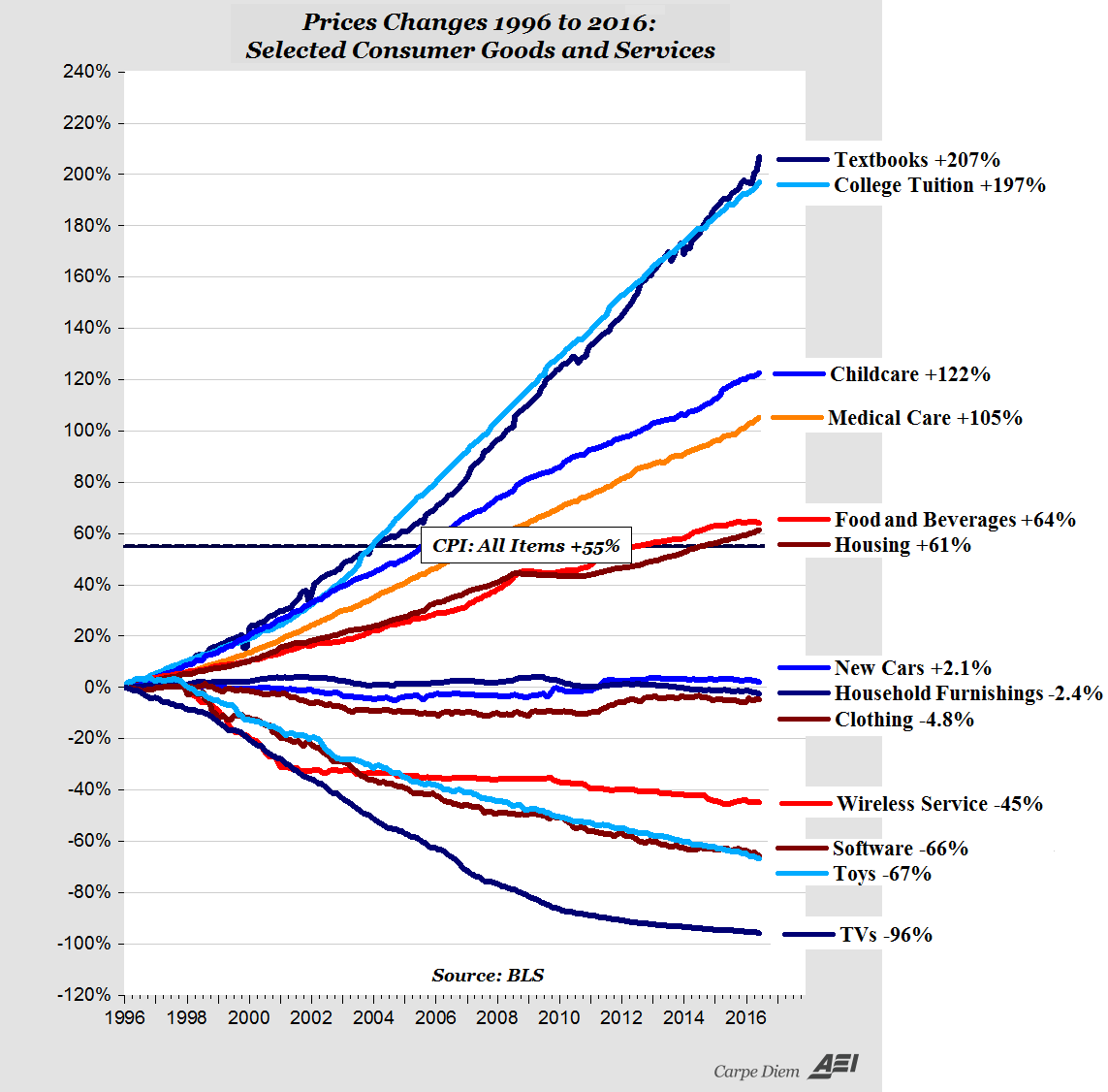

As you might have heard, many people equate capitalism with being “good for big business.” But capitalism is great for the consumer. When you look at these changes, capitalism feels much more like a miracle we should celebrate than a scourge we should demonize. Take a look at the chart below:

This chart outlines how prices have changed in various industries over the past 20 years. What stands out is that, in every market in which sellers must compete fiercely to win, technology (especially software) has a natural tendency to lower prices. As American entrepreneur Marc Andreessen has observed:

So you’ve got these sectors of the economy where there’s rapid productivity growth. Prices are falling fast. Those are the industries where everyone is worried that the jobs are going away—or to China or Japan or Mexico. People say there’s too much disruption—too much technological change. The Silicon Valley kids are wreaking havoc on the economy.

Then you have the sectors in which prices are rapidly rising: health care, education, construction, prescription drugs, elder care and child care. Here there’s very little technological innovation. Those are sectors with insufficient productivity growth, innovation, and disruption. You’ve got monopolies, oligopolies, cartels, government-run markets, price-fixing—all the dysfunctional behaviors that lead to rapid increase in prices.

The government injects more subsidies into those markets, but because those are inelastic markets, the subsidies just cause prices to go up further, which is what is happening with higher education.

Yes, capitalism indeed lowers prices.

Capitalism Is Unselfish

If you wish to prosper, let your customer prosper.

~Frederic Bastiat

This is probably the hardest claim to swallow. After all, maybe the greatest insight Adam Smith (the author of the Bible of Economics, The Wealth of Nations) offered was the power of self interest! As he put it:

It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest.

In other words, capitalism understands incentives, or the idea that people are naturally selfish. A person doesn’t create a business out of the kindness of their heart. They do it to feed themselves and their families. This selfishness is immeasurably powerful.

But in order to successfully create and sell a product, a businessman must actually look outside his own needs and consider the needs of the customer. A businessman has to create value for others before capturing value for himself. As a result, capitalism is the greatest incentive system in the world for focusing on others and their needs. And the result of that is empathy, understanding, and peace. Often, an entrepreneur’s net worth is merely the register of how much he has improved the lives of his fellow human beings.

I’ll summarize this section with two more quotes, the first from Milton Friedman:

The great virtue of a free market system is that it does not care what color people are; it does not care what their religion is; it only cares whether they can produce something you want to buy. It is the most effective system we have discovered to enable people who hate one another to deal with one another and help one another.

And the second from John Maynard Keynes:

Dangerous human proclivities can be canalised into comparatively harmless channels by the existence of opportunities for money-making and private wealth, which, if they cannot be satisfied in this way, may find their outlet in cruelty, the reckless pursuit of personal power and authority, and other forms of self-aggrandizement. It is better that a man should tyrannize over his bank balance than over his fellow-citizens; and whilst the former is sometimes denounced as being but a means to the latter, sometimes at least it is an alternative.

Now, you might say, if all this is true, and capitalism is so great, why is the world doing so poorly? Shouldn’t people be getting wealthier from trade? Shouldn’t technologies be increasing our standard of living?

To which the answers are: It’s not doing poorly. Yes. And yes.

Global poverty is at its lowest point ever:

"The proportion of the world’s population living in extreme poverty has fallen below 10%." https://t.co/Oin9AgINpr pic.twitter.com/Sa5dqN7WAd

— cdixon.eth (@cdixon) January 16, 2016

Life expectancy is at its highest point ever:

In 20 years (1991-2011), most developed countries in the world gained 4-5 years in life expectancy. That's amazing. https://t.co/Opx6FzSzad

— Vignir Gudmunds (@vignirio) August 25, 2016

And much of the improvement in quality of life is due to technology:

Technological change explains about 80% of the decrease in under-5 mortality across countries

— Stefan Thewissen (@ThewissenS) June 22, 2016

JHE 48: 16-25 pic.twitter.com/IpNIPyprYV

Also, people are wealthier (we enjoy a higher standard of living), as a whole, than ever before:

Average Americans in 2016 were richer than Rockefeller in 1916. Here's how... https://t.co/orDYfNvLhn #HumanProgressData pic.twitter.com/SBFEFwifwX

— Cato Institute (@CatoInstitute) March 1, 2019

Lastly, the linchpin: every country that adopts this system of free trade, competition, and entrepreneurship is a rich country:

There is no country with high economic freedom that is poor h/t @MaxCRoser https://t.co/oRMETUJH3Y pic.twitter.com/AMar6jnf5G

— Ninja Economics (@NinjaEconomics) June 20, 2016

Objections

It would not be intellectually honest to present the case for capitalism without acknowledging the most common objections. The same economics class that teaches me the irrefutable truth of free trade also teaches me about tradeoffs. And capitalism has plenty of tradeoffs.

I’ve already discussed one: that trading with global partners often means losing jobs to them. Here are three more:

Capitalism Causes Wealth Inequality. While it’s true that inequality is increasing in the US, global wealth inequality is actually decreasing (because globally the very, very poor are getting wealthier at a much quicker rate than the rich are getting richer). I do suspect inequality is a real tradeoff of capitalism in the long-run, however. But as Winston Churchill observed: “The inherent vice of capitalism is the unequal sharing of blessings. The inherent virtue of socialism is the equal sharing of miseries.”

Capitalism Causes Wealth to Be Concentrated in the Hands of Just a Few. “Bad” wealth concentration often results from monopolies, which capitalism is extremely effective at removing. “Good” concentrated wealth—earned through truly breakthrough innovation (like Bill Gates’s wealth, for example)—is great and should be celebrated. Gates ought to be rewarded for all the value he’s created, and society should encourage it. And, by the way, look at all the good he does with that wealth:

Bill Gates will be paying off $76 million of Nigeria's debt after the country met polio vaccination targets. pic.twitter.com/Gv7bkROXXH

— The Spectator Index (@spectatorindex) March 3, 2018

Capitalism Incentivizes Business Owners to Pay Workers as Little as Possible. Employees simply trade with employers when they agree to work (trading their time and skills for a paycheck), and gains from trade certainly apply. Any worker who freely accepts a minimum-wage job from, say, Walmart, deems himself better off for doing so, otherwise he wouldn’t do it. Remember the principle: behind every fair trade, both parties get what they want. Just like a country must work its way up the opportunity-cost ladder from a manufacturing economy (producing goods like t-shirts and trinkets) to a services economy (producing goods like consulting and banking), workers must improve their value in the marketplace through education, specialization, and training. Also, just as firms compete with each other over consumers, they compete with each other over workers. If Wal-Mart is underpaying a great employee, and Costco believes that by offering an extra dollar per hour it will steal that employee from Walmart, capitalism says Costco will do it. Look no further than Silicon Valley to see the lengths companies will go to persuade scarce talent to work for them. Competition actually benefits the scarce worker, as it should. And it pays a commodity price for a commodity worker, as it should.

Nicola Wright

Nicola Wright

The genius of (and challenge for) America is that it provides a system that allows everyone equality of opportunity to succeed in moving from a commodity worker to a scarce worker. We have a long way to go here. I don’t think anything I’ve written here is controversial, although there may be some disagreements at the margins. And if you don’t buy my arguments, take note of hyper-capitalist Barack Obama, recently quoted in the Economist:

It is important to remember that capitalism has been the greatest driver of prosperity and opportunity the world has ever known.

Thanks, Obama. Calzones are pretty tasty after all.

This is a slightly edited version of an article published on Medium in 2016.

Keep reading

Capturing the ‘Odyssey’

Biting the Hand

Sex Differences Above the Neck

A Beautiful Odyssey, Made Dreary By Remorse

Men Without Meaning